Newspapers and clickbait 24-7 news websites, desperate for clicks, are peddling a story of a doomsday time for the economy, particularly the property market, as interest rates and inflation create the perfect storm for the UK property market.

Doom and gloom in the British property market or clickbait doom-mongers?

Newspapers and clickbait 24-7 news websites, desperate for clicks, are peddling a story of a doomsday time for the economy, particularly the property market, as interest rates and inflation create the perfect storm for the UK property market.

So, let us look at what is happening in the British property market and whether house prices will drop.

Yes - Lewisham house prices will be lower in 24 months.

Yet the reductions in what I believe a property will sell for in the next couple of years compared to the doom-mongers is wildly different.

The doom-mongers are saying the 2022 property market will be like the crash years of 1988 and 2008.

I'm afraid I have to disagree, let me explain what the difference is this time compared to the previous house price crashes.

To start with …

56.25% of homeowners don’t have a mortgage, whilst in 1988, that was 35.8%. These people are shielded from the interest rate rises.

The next point is negative equity.

Yes, negative equity was an issue after 1988 when everyone had an endowment mortgage, so they never paid any of the capital off their mortgage. Therefore, when house prices dropped, negative equity was a massive issue as people owed more than what their house was worth.

By 2008, nobody was taking out endowment mortgages, yet still, 1 in 2 were interest-only mortgages (meaning the capital wasn’t being paid off). Today, 17 out of 20 homeowners are on repayment mortgages - so they have more home equity, so negative equity isn't so much an issue.

The issue is the increasing interest rates. Yes, they are rising … albeit from artificially low rates.

In 1988, nearly everyone was on a variable rate mortgage and an average mortgage interest rate was 10.8%, and they rose to 16.4% by 1990. That hurt, yet most survived.

In 2008, 6 out of 10 homeowners had learned their lesson and were on fixed rates at an average rate of 6.07%. Today 17 out of 20 homeowners have long-term fixed rates with an average of 2.14%.

Also, it must be noted that homebuyers have been stress tested for 6% to 7% mortgage rates since 2014 because of the Bank of England MMR rule changes. It will be challenging, and lifestyle choices will need to be made, yet we should not see the dumping of houses on the market as we did in 2008/9.

The next issue is the number of mortgages being pulled. Yes, around 1,000 mortgage deals have been removed in the last week - yet there are still 3,000+ deals out there … and most are still fixed rates.

Also, let’s not forget that 1 in 5 people rent today and are protected from all this, yet in 1988, only 1 in 14 rented.

Therefore, the economic conditions surrounding the house price crash

in 1988 and 2008 are not there now.

Don’t get me wrong, those homeowners coming off their fixed rates of around 2% in the coming years will have to make tough choices as they will see their monthly mortgage payments rise substantially.

Yet, as I have discussed in other articles, extending your mortgage term can significantly affect your monthly mortgage payments and there are things that homeowners should be doing now to mitigate the issue in the coming few years.

But back to the question, should people wait to move, and what

will happen to Lewisham property prices?

I believe that subject to nothing seismic happening in the world, Lewisham property values will be broadly neutral and slowly drift downwards over the next 24 months. I believe they will drift because of the issues of inflation and mortgage affordability, yet we won’t have a crash for the points made in the first part of this article. I believe Lewisham property will be selling for sums of 4% to 6% less in a couple of years compared to today.

This means if we achieve prices of 4% to 6% less, homeowners will still be getting the same prices the property market was getting in the summer of 2021 – again – nobody was complaining about those!

However, let us assume I am wrong with my thoughts, and we see a significant house price crash; what then?

Well, let me look at the last two house price crashes first.

The housing crash of 1988 saw the average house in the UK drop from £63,784 to £50,167, a drop of 20.09%.

The housing crash of 2008 saw the average house in the UK drop from £184,132 to £154,065, a drop of 16.33%.

So, let’s assume that Lewisham house prices fall by 18% -

surprisingly, it will not help Lewisham buyers.

In previous house price crashes, people tend to find their careers are more at risk, and in turn, their wages don't rise as much. It is the younger generation (i.e., first-time buyers age range) that often gets hit the toughest by these recessions.

Let me look at Lewisham first-time buyers.

If Lewisham first-time buyers wait until 2024 to buy and Lewisham property values drop by 18%, that will prove more expensive. Let me explain why …

In the last property crash of 2008, lenders withdrew 5% deposit mortgages. The smallest mortgage that first-time buyers could obtain was with a 10% deposit, and even those were hard to come by.

When writing this article, first-time buyers can obtain a 5% deposit mortgage for a fixed rate of 3.92% for five years.

The typical first-time buyer apartment in Lewisham sells for £367,716.

If first-time buyers were to buy now, on this mortgage deal, they would have to find an £18,386 deposit, and their monthly mortgage payments would be £1,530.03 per month.

So, let’s say property values in Lewisham do drop by 18% in the next 24 months; the apartment would now be worth £301,527, a significant saving in the purchase price.

Or is it?

Everyone believes the Bank of England will raise interest rates further, so let's assume they go to 5.5% by the autumn of 2024. That will mean the rate for a 10% deposit first-time buyer mortgage will be in the early 7%’s, so let me assume 7.19% (because the lenders have in the past increased the gap between the Bank of England base rate and the mortgage rate in more challenging economic times to allow for the extra risk).

The monthly mortgage payment in two years on the 7.19% mortgage would be £1,769.97 per month, and in those two years, you would have had to have saved an additional £11,767 to make up your 10% deposit of £30,153.

So even if Lewisham's house prices did drop by 18%, the first-time buyer would be £2,879 worse off a year in mortgage payments

(and would have to save many thousands extra for their deposit)

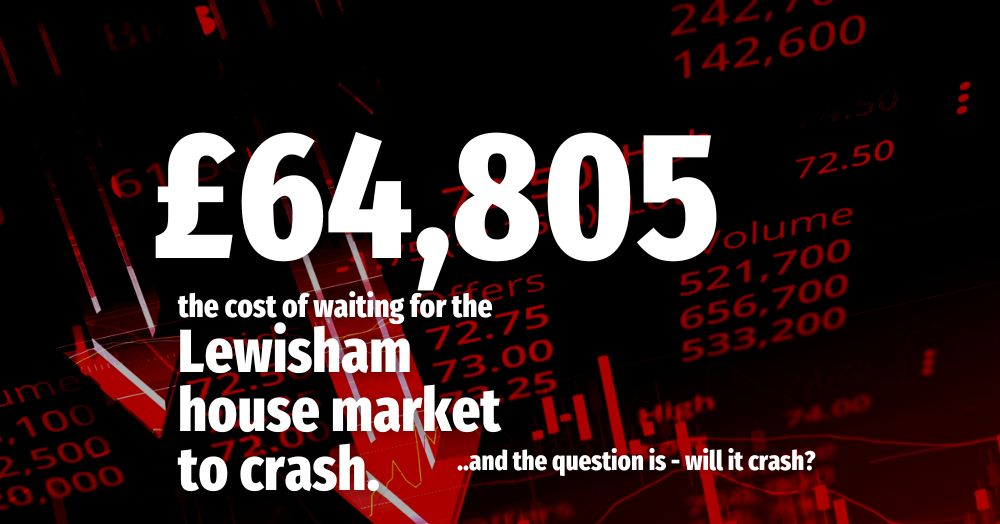

... and then there is the other cost of waiting.

You have two years’ worth of rent to pay. The average rent for a Lewisham property is £1,850 per month.

If you waited a couple of years for Lewisham house prices to drop by 18%, you would spend £44,400 in rent plus have higher mortgage payments in 2024/5/6 and with the extra deposit mentioned above it would add up to an additional £64,805 over the next five years.

Yes, the price you paid for your Lewisham home would be lower if you waited two years. Yet, you would only benefit from that when you sold on versus the economic pain of two years of extra renting, the higher deposit and higher mortgage payments in a couple of years.

This doesn't even consider the emotional cost of putting your life on hold for two years, and there is no guarantee that the mortgage lending criteria in two years would allow you to step onto the property ladder.

So, now I have shown that waiting will cost you financially and emotionally, what are your thoughts on the matter?

Lewisham house prices will drop, yet did you realise it will cost you more, even if house prices are falling?

Do you believe the doom-mongers, or do you believe in the robust nature of the British economy?

Don’t forget, George Osbourne said house prices would drop by 18% in May 2016 if we voted to leave the European Union, whilst many economists said house prices would fall by 5% to 10% when Covid hit in March 2020.

And we all know what happened to those predictions now.

If you believe you will be better off owning your own Lewisham home rather than renting one, don't bother to wait for the suggested house price crash that may never happen.

These are my thoughts - what are yours? Let me know in the comments.

Written By

Neil Raja ANAEA, MARLA

Director

M 07930501099

P 02088524441

E neil.raja@remax.co.uk

Remax First

250 Lewisham High Street, London, Se13 6Ju

www.remax-first.lifesycle.co.uk/blogs

𝗖𝗹𝗶𝗰𝗸 𝗜𝗺𝗮𝗴𝗲 𝘁𝗼 𝗠𝗲𝘀𝘀𝗮𝗴𝗲 𝗠𝗲 𝗗𝗶𝗿𝗲𝗰𝘁𝗹𝘆

𝗖𝗹𝗶𝗰𝗸 𝗜𝗺𝗮𝗴𝗲 𝘁𝗼 𝗠𝗲𝘀𝘀𝗮𝗴𝗲 𝗠𝗲 𝗗𝗶𝗿𝗲𝗰𝘁𝗹𝘆 𝐑𝐄𝐀𝐃 𝐌𝐎𝐑𝐄

by

by

Share this with

Email

Facebook

Messenger

Twitter

Pinterest

LinkedIn

Copy this link